UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number

(Exact name of registrant as specified in its charter) |

|

||

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

|

|

|

|

|

|

|

||

(Address of principal executive offices) |

|

(Zip code) |

(

(Registrant’s telephone number, including area code)

Not Applicable

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

Name of exchange |

Title of each class |

|

Trading Symbol |

|

on which registered: |

|

|

The |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

☐ |

Accelerated filer |

☐ |

☒ |

Smaller reporting company |

||

|

|

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

The aggregate market value of the voting stock held by non-affiliates of the registrant as of June 30, 2024 was approximately $

There were

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for its 2025 Annual Meeting of Stockholders (the “Proxy Statement”), to be filed within 120 days of the registrant’s fiscal year ended December 31, 2024, are incorporated by reference in Part III of this Annual Report on Form 10-K. Except with respect to information specifically incorporated by reference in this Annual Report on Form 10-K, the Proxy Statement is not deemed to be filed as part of this Annual Report on Form 10-K.

ASP Isotopes Inc.

Annual Report on Form 10-K

For the Year Ended December 31, 2024

Table of Contents

2

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains "forward-looking statements" within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. All statements other than statements of historical fact contained in this Annual Report on Form 10-K, including statements regarding our future results of operations and financial position, business strategy and plans and objectives of management for future operations, are forward-looking statements. These statements involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements.

In some cases, you can identify forward-looking statements by terms such as “may,” “should,” “would,” “expects,” “plans,” “anticipates,” “could,” “intends,” “target,” “projects,” “contemplates,” “believes,” “estimates,” “predicts,” “potential” or “continue” or the negative of these terms or other similar expressions. The forward-looking statements in this Annual Report on Form 10-K are only predictions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition and results of operations. These forward-looking statements speak only as of the date of this Annual Report on Form 10-K and are subject to a number of risks, uncertainties and assumptions described in the section titled “Risk Factors” and elsewhere in this Annual Report on Form 10-K. Because forward-looking statements are inherently subject to risks and uncertainties, some of which cannot be predicted or quantified, you should not rely on these forward-looking statements as predictions of future events. The events and circumstances reflected in our forward-looking statements may not be achieved or occur and actual results could differ materially from those projected in the forward-looking statements. Some of the key factors that could cause actual results to differ from our expectations include:

3

These statements relate to future events or to our future financial performance and involve known and unknown risks, uncertainties, and other factors that may cause our actual results, performance, or achievements to be materially different from any future results, performance, or achievements expressed or implied by these forward-looking statements. Factors that may cause actual results to differ materially from current expectations include, among other things, those set forth in Part I, Item 1A - “Risk Factors” below and for the reasons described elsewhere in this Annual Report on Form 10-K. Any forward-looking statement in this Annual Report on Form 10-K reflects our current view with respect to future events and is subject to these and other risks, uncertainties, and assumptions relating to our operations, results of operations, industry, and future growth. Given these uncertainties, you should not place undue reliance on these forward-looking statements. Except as required by law, we assume no obligation to update or revise these forward-looking statements for any reason, even if new information becomes available in the future.

This Annual Report on Form 10-K also contains estimates, projections, and other information concerning our industry, our business, and the potential markets for certain isotopes, including data regarding the estimated size of those markets, their projected growth rates, and the incidence of certain medical conditions. Information that is based on estimates, forecasts, projections, or similar methodologies is inherently subject to uncertainties, and actual events or circumstances may differ materially from events and circumstances reflected in this information. Unless otherwise expressly stated, we obtained these industry, business, market, and other data from reports, research surveys, studies, and similar data prepared by third parties, industry, medical and general publications, government data, and similar sources. In some cases, we do not expressly refer to the sources from which these data are derived.

Except where the context otherwise requires, in this Annual Report on Form 10-K, “we,” “us,” “our,” “ASP Isotopes,” and the “Company” refer to ASP Isotopes Inc. and, where appropriate, its consolidated subsidiaries.

Trademarks

All trademarks, service marks, and trade names included in this Annual Report on Form 10-K are the property of their respective owners. Solely for convenience, the trademarks and trade names in this report may be referred to without the ® and ™ symbols, but such references should not be construed as any indicator that their respective owners will not assert, to the fullest extent under applicable law, their rights thereto.

PART I

Item 1. Business

Overview

We are a development stage advanced materials company dedicated to the development of technology and processes that, if successful, will allow for the enrichment of natural isotopes into higher concentration products, which could be used in several industries. Our proprietary technologies, the Aerodynamic Separation Process (“ASP technology”) and Quantum Enrichment

4

technology (“QE technology”), are designed to enable the production of isotopes used in several industries. Our initial focus is on the production and commercialization of enriched Carbon-14 (“C-14”), Silicon-28 (“Si-28”) and Ytterbium-176 (“Yb-176”).

We have completed the commissioning phase and are commencing commercial production at our C-14 and Si-28 enrichment facilities in Pretoria, South Africa. We are in the process of commissioning and commencing commercial production at our Yb-176 enrichment facility in Pretoria, South Africa. Our C-14 and Si-28 enrichment facilities utilize the ASP technology and our Yb-176 enrichment facility utilizes QE technology. We expect our first three enrichment facilities to generate commercial product during 2025. In addition, we have started planning additional isotope enrichment plants both in South Africa and in other jurisdictions, including Iceland and the United States. We believe the C-14 we may produce using the ASP technology could be used in the development of new pharmaceuticals and agrochemicals. We believe the Si-28 we may produce using the ASP technology may be used to create advanced semiconductors and in quantum computing. We believe the Yb-176 we may produce using the QE technology may be used to create radiotherapeutics that treat various forms of oncology.

In addition, we are considering the future development of the ASP technology for the separation of Zinc-68 and Xenon-129/136 for potential use in the healthcare end market, Germanium 70/72/74 for potential use in the semiconductor end market, and Chlorine -37 for potential use in the nuclear energy end market. We are also considering the future development of QE technology for the separation of Nickel-64, Gadolinium-160, Ytterbium-171, Lithium 6 and Lithium7.

We are currently pursuing an initiative to apply our enrichment technologies to the enrichment of Uranium-235 (“U-235”) in South Africa. We believe that the U-235 we may produce using quantum enrichment technology may be commercialized as a nuclear fuel component for use in the new generation of high-assay low-enriched uranium (HALEU)-fueled small modular reactors that are now under development for commercial and government uses. In furtherance of our uranium enrichment initiative, in October 2024, we entered into a term sheet with TerraPower, LLC which contemplates the parties entering into definitive agreements pursuant to which TerraPower would provide funding for the construction of a HALEU production facility and agree to purchase all HALEU produced at the facility over a 10-year period after the planned completion of the facility in 2027. In addition, in November 2024, we entered into a memorandum of understanding with The South African Nuclear Energy Corporation (Necsa), a South African state-owned company responsible for undertaking and promoting research and development in the field of nuclear energy and radiation sciences, to collaborate on the research, development and ultimately the commercial production of advanced nuclear fuels. Subject to the receipt of funding and all required permits and licenses to begin enrichment of U-235 in South Africa, it is anticipated that the research, development and ultimate construction of a HALEU production facility will take place at South Africa’s main nuclear research center at Pelindaba in Pretoria.

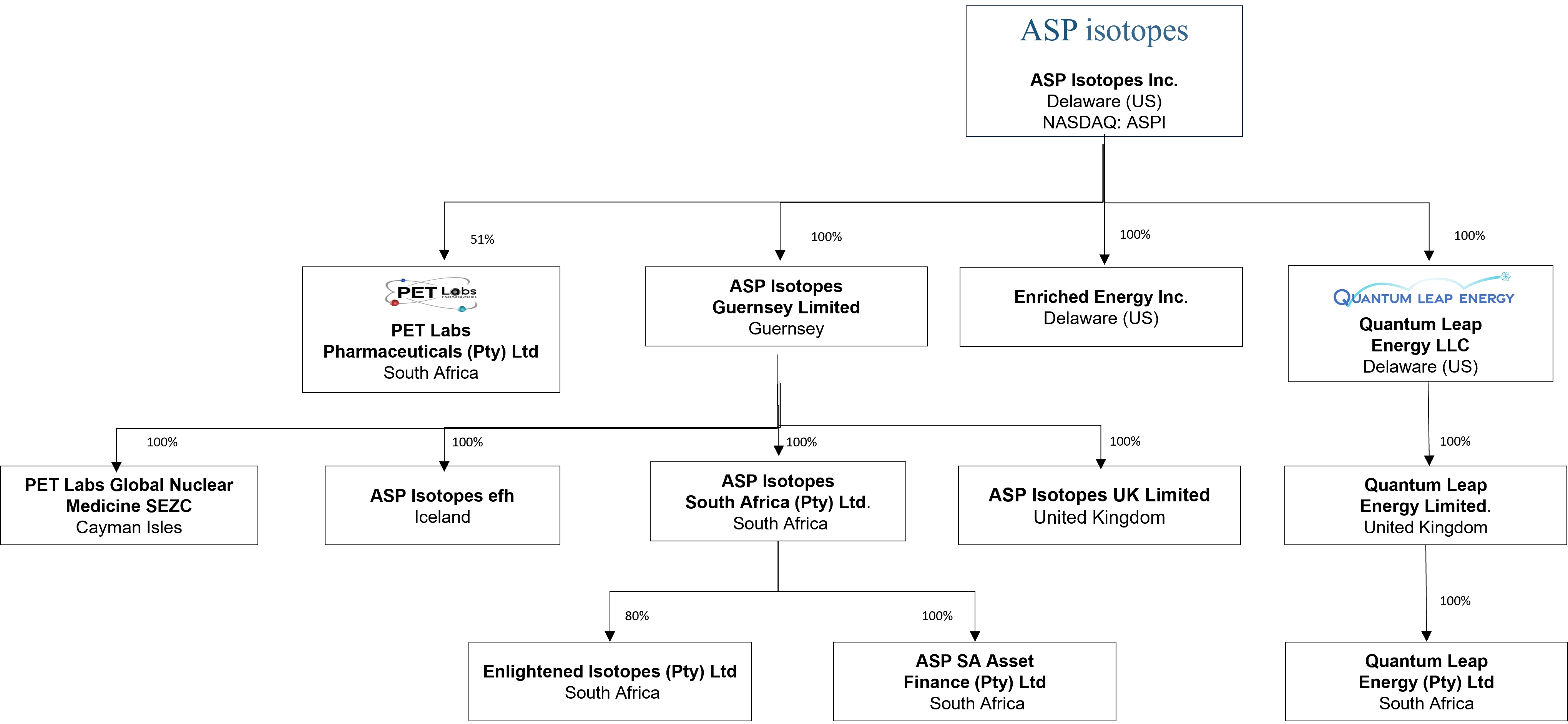

We operate principally through subsidiaries. ASP Isotopes Guernsey Limited (the holding company of ASP Isotopes South Africa (Proprietary) Limited, Enlightened Isotopes (Pty) Ltd) and ASPI South Africa Asset Finance (Pty) Ltd, which will be focused on the development and commercialization of high-value, low-volume isotopes for highly specialized end markets (such as C-14, Si-28 and Yb-176). In September 2023, we formed a new subsidiary, Quantum Leap Energy LLC, which also has a subsidiary in the United Kingdom (Quantum Leap Energy Ltd), to focus on the development and commercialization of advanced nuclear fuels such as HALEU and Lithium-6. ASP Isotopes UK Ltd is the owner of our technology. In addition, we have a 51% ownership stake in PET Labs Pharmaceuticals Proprietary Limited (PET Labs), a South African radiopharmaceutical operations company focused on the production of fluorinated radioisotopes and active pharmaceutical ingredients, through which we entered the downstream medical isotope production and distribution market.

5

Our corporate structure and ownership of our subsidiaries is set forth in the chart below:

Our Segments

As of December 31, 2023, we managed our operations as a single segment, specialist isotopes and related services. Beginning in 2024, primarily as a result of the increased business activities of our subsidiary, Quantum Leap Energy LLC, we manage our operations as two operating segments: (i) nuclear fuels, and (ii) specialist isotopes and related services:

Our Strategy

Commence commercial production at each of our enrichment facilities in Pretoria, South Africa.

We commenced commercial production of enriched isotopes at our ASP enrichment facilities located in Pretoria, South Africa during the first quarter of 2025. Our first ASP enrichment facility is designed to enrich light isotopes, such as Carbon-14. The second ASP enrichment facility, which is substantially larger than the first, should have the potential to enrich kilogram quantities of relatively heavier isotopes, including but not limited to Silicon-28 and Molybdenum-100. We anticipate shipping the first commercial batches of enriched Carbon-14 in mid-2025 and enriched Silicon-28 during the second quarter of 2025. We are in the process of commissioning and commencing commercial production at our third enrichment facility, a QE technology facility, which will be our first laser-based enrichment plant and is expected to be able to achieve a 99.75% enrichment for Ytterbium-176. We expect to commence commercial production of Ytterbium-176 during the second quarter of 2025.

Demonstrate the capability to produce commercial quantities of enriched C-14, Si-28 and Yb-176 using the ASP and QE technologies and capitalize on the opportunity to solve many supply chain challenges that currently exist.

We intend to demonstrate the capability to produce C-14, Si-28 and Yb-176 at a scale that can support anticipated customer demand for all three isotopes.

Historically, Russia has been the sole supplier of C-14, which is used as a tracer in the development of new pharmaceuticals and agrochemicals. The supply chain has been inherently fragile with inconsistent service. We have received an initial supply of feedstock from our customer and have started the enrichment of C-14.

6

Isotopically enriched silicon is regarded as a promising material for semiconductor quantum information due to its very long coherence times and its compatibility with the readily available industrial platform. We believe that the ASP technology is ideally suited to the production of this isotope because it has the ability to enrich molecules of low molecular mass. Other electronic gasses that can likely be enriched using ASP Technology include disilane and germane.

Enriched Ytterbium-176 can be irradiated to produce Lutetium-177, which has been identified for use in oncology, particularly in targeted radionuclide therapy ("TRT"). TRT is used in the treatment of various types of cancers, including neuroendocrine tumors, prostate cancer, and bone metastases, among others. There are numerous ongoing clinical trials studying Lutetium-177 PSMA-617 in patients with metastatic castration-resistant prostate cancer. We have obtained all necessary licenses within South Africa to proceed with the commercial development of this product.

Continue identifying potential offtake customers and strategic partners for our enriched isotopes.

We have significant interest from potential offtake customers for the enriched isotopes that we intend to produce. In June 2023, we entered into a tolling agreement with a Canadian customer for the entire capacity of our C-14 production facility. In April and June 2024, we entered into purchase orders with a US semiconductor company and a global industrial gas company for the supply of highly enriched silicon-28. We are currently in discussions with potential customers that have an interest in entering into long-term supply agreements for kilogram quantities of Si-28 and larger quantities of Xe-129, Ge 72, Ge-74, Zn-68, and Cl-37. We intend to identify additional potential customers and strategic partners for isotopes that we may produce at our existing and planned enrichment facilities.

Demonstrate the capability to produce high-assay low-enriched uranium (HALEU) using our enrichment technologies and meet anticipated demand for the new generation of HALEU-fueled small modular reactors and advanced reactor designs that are now under development for commercial and government uses.

We plan to begin research and development for the enrichment of uranium to demonstrate our capability to produce HALEU using Quantum Enrichment technology. We anticipate a future demand for HALEU for the new generation of HALEU-fueled small modular reactors ("SMRs") and advanced reactor designs that are now under development for commercial and government uses. SMRs are viewed as being cheaper, safer, and more versatile than traditional large-scale nuclear reactors, and development of the new technology is receiving considerable funding from the U.S. Department of Energy, as well as from the governments of other countries. There is currently no commercial production of HALEU in the United States. We are currently conducting a feasibility study with respect to constructing an enrichment facility in South Africa, the U.S. and the United Kingdom. We are currently in discussions with nuclear regulatory authorities in multiple countries, including the UK Atomic Energy Authority, UK Office of Nuclear Regulation (ONR), Nuclear Energy Corporation of South Africa (NECSA), the South African Department of Mineral Resources and Energy (DMRE), United States Department of Energy (DOE) and the United States Nuclear Regulatory Commission (NRC), regarding the construction of a nuclear fuel plant in these countries.

We intend to progress our uranium enrichment initiative first in South Africa. In November 2024, we entered into a Memorandum of Understanding ("MOU") with The South African Nuclear Energy Corporation (Necsa) to collaborate on the research, development and ultimately the commercial production of advanced nuclear fuels. Necsa is a state-owned company established by the Republic of South Africa Nuclear Energy Act in 1999 with a mandate to undertake and promote research and development in the field of nuclear energy and radiation sciences. Necsa is also responsible for processing source material, and co-operating with other institutions on nuclear and related matters. The proposed structure under discussion for the delivery of the objectives of the MOU contemplates the formation of a new entity in South Africa with a board of directors consisting of at least two representatives from ASPI and Necsa. It is anticipated that the research, development and ultimate construction of a HALEU production facility will take place at South Africa’s main nuclear research center located at Pelindaba, Pretoria.

Alongside our talks with regulators, we are currently discussing with multiple counterparties engaged in the development of SMR reactors to produce HALEU to further their research efforts and future commercial endeavors. We have entered into two MOUs with US-based SMR companies for the supply of HALEU. For example, our term sheet with TerraPower, LLC which contemplates the parties entering into definitive agreements pursuant to which TerraPower would provide funding for the construction of a HALEU production facility and agree to purchase all HALEU produced at the facility over a 10-year period after the planned completion of the facility in 2027.

Demonstrate the effectiveness and value in the use of stable isotopes in the downstream radiopharmacy market, after acquiring 51% ownership interest in PET Labs, the leading radiopharmacy in South Africa. This investment will address the radioisotope needs of South Africa as well as certain neighboring countries.

Under the terms of a Share Purchase Agreement, dated October 30, 2023, we acquired 51% of the issued share capital of PET Labs Pharmaceuticals Proprietary Limited, a company incorporated in the Republic of South Africa (“PET Labs”). PET Labs is a South African radiopharmaceutical operations company, dedicated to nuclear medicine and the science of radiopharmaceutical

7

production. As a result of this transaction, we entered into the downstream radiopharmacy market that we intend to service in the future. This transaction will help provide the market with adequate proof of concept of the value of utilizing Mo-100 in downstream SPECT imaging procedures while providing supply chain stability to the region of South Africa and neighboring countries. We intend to expand PET Labs’ existing operations by adding two new cyclotrons to its service footprint, enabling the company to properly expand its other revenue generation mediums, which is anticipated to drive free cash flow to the company.

Our Strengths

ASP technology initially developed by Klydon and further developed by ASP Isotopes Inc..

The aerodynamic separation technique has its origins in the South African uranium enrichment program in the 1980s, and the ASP technology had been developed during the last two decades by the scientists at Klydon. The scientists at Klydon had constructed two ASP plants for the enrichment of oxygen-18 and silicon-28 in Pretoria, South Africa, which were commissioned in October 2015 and July 2018, respectively. While the technology has not yet been used to enrich either Uranium or heavier isotopes, we believe the success of the enrichment process for oxygen-18 and silicon-28 has demonstrated the efficacy and commercial scalability of the ASP technology. If our research and development is successful (and subject to obtaining applicable regulatory approvals and appropriate licenses), we plan to commercialize many different isotopes produced using the ASP technology. To date, we have not produced commercial quantities of any enriched isotopes and we have not demonstrated the ability to produce any enriched isotopes in commercial quantities using ASP technology.

Extensive Research and Development Experience in Aerodynamic Separation Technology and Processes.

Subject to successful research and development, our ASP technology has the potential to produce many different types of isotopes. Klydon had spent the last two decades and tens of millions of dollars developing the aerodynamic separation technique used in the ASP technology, generating critical trade secrets. We believe our competitors lag behind us in terms of the technical expertise of our senior management and the know-how contained in the aerodynamic separation technique and will be unable to replicate the expected results of the ASP technology, even as we expect to continue to improve the existing technology and processes. Additionally, the high capital costs of development of proprietary technologies, significant lead times required to construct new enrichment facilities, as well as stringent regulatory and operating requirements applicable to enrichment facilities, adds to the significant barriers to entry for smaller competing market participants.

ASP technology is a flexible platform with the potential to produce many different isotopes that could serve large addressable markets.

ASP technology is a flexible platform, compact in size and weight, and could be easily scaled to an industrial level with number of separation devices added in parallel. The ASP technology also has few moving parts, with low capital and operating costs in comparison to alternatives. The technology is particularly efficient at enriching isotopes of low atomic mass. We believe that, assuming receipt of required regulatory approvals and governmental permits, the ASP technology can be deployed quickly and with a relatively minimal capital cost, to enrich many different isotopes that we believe consumers require both today and in the future in end markets such as healthcare, technology and energy.

The ASP technology is designed to be scalable, low cost, low energy, and environmentally friendly, with no radioactive waste or hazardous materials produced in the process and planned arrangements to reuse chemical by-products.

QE technology has the potential to produce many different enriched isotopes that cannot be enriched using ASP Technology.

Our QE technology is potentially a highly efficacious enrichment technology with the greatest enrichment factor of any enrichment process. In laboratory tests our scientists have achieved enrichment factors of up to 678 which compares to enrichment factors of less than 50 for AVLIS and 1.15 for a traditional centrifuge. QE can also be used to enrich elements where there is no known gaseous form of that element. We have completed the construction of our first QE enrichment facility in Pretoria, South Africa where we intend to produce 99.75% enriched Ytterbium-176.

Experienced team

Our board of directors and advisers have specialized expertise in isotope enrichment, research and development, technology, plant development, and manufacturing. Dr Hendrik Strydom, our chief technology officer and one of our directors, previously co-founded Klydon and has over 40 years of experience in isotope enrichment and laser design and manufacture. The scientific team that joined our company from Klydon combined has decades of experience in research and development of isotope enrichment and amassed deep knowledge in the field.

8

Our board of directors and our management team also have broad experience and successful track records in fusion technology and fusion materials, biopharmaceutical research, chemicals, manufacturing and commercialization, as well as in business, operations, and finance. Our board of directors’ and management team’s experience was gained at leading companies and financial institutions that include, Bear Stearns, Deutsche Bank, Highbridge Capital, Investec Bank, Morgan Stanley and Soros Fund Management.

Technical Background

What are Isotopes?

Isotopes are two or more types of atoms that have the same atomic number (number of protons in their nuclei) and position in the periodic table (and hence belong to the same chemical element), and that differ in nucleon numbers (mass numbers) due to different numbers of neutrons in their nuclei. While all isotopes of a given element have almost the same chemical properties, they have different atomic masses and physical properties.

The number of protons within the atom’s nucleus is called atomic number and is equal to the number of electrons in the neutral (non-ionized) atom. Each atomic number identifies a specific element, but not the isotope; an atom of a given element may have a wide range in its number of neutrons. The number of nucleons (both protons and neutrons) in the nucleus is the atom’s mass number, and each isotope of a given element has a different mass number. For example, carbon-12, carbon-13, and carbon-14 are three isotopes of the element carbon with mass numbers 12, 13, and 14, respectively. The atomic number of carbon is 6, which means that every carbon atom has 6 protons so that the neutron numbers of these isotopes are 6, 7, and 8 respectively.

There are 23 isotopes of Silicon, all of which have 14 protons and between 8 and 30 neutrons. The table below shows a selection of those isotopes. Three isotopes are stable which have mass numbers of 28, 29 and 30 which have 14, 15 and 16 neutrons respectively. The other 20 isotopes are radioactive and decay with short half-lives and are therefore do not typically exist in naturally occurring silicon. In naturally occurring silicon, the isotope with atomic mass of 28 is usually the most abundant, typically accounting for approximately 92.22% of the material. The isotope with atomic mass of 29 typically accounts for 4.69% of the material and the isotope with atomic mass of 30 typically accounts for 3.09% of the material.

Molybdenum has 33 known isotopes, ranging in atomic mass from 83 to 115, as well as four metastable nuclear isomers. Seven isotopes occur naturally, with atomic masses of 92, 94, 95, 96, 97, 98, and 100. All unstable isotopes of molybdenum decay into isotopes of zirconium, niobium, technetium, and ruthenium.

Uranium is a naturally occurring radioactive element that has no stable isotope. It has two primordial isotopes, uranium-238 and uranium-235, which have long half-lives and are found in appreciable quantity in the Earth’s crust. The decay product, uranium-234 is also found. Other isotopes such as uranium-233 have been produced in breeder reactors. In addition to isotopes found in nature or nuclear reactors, many isotopes with far shorter half-lives have been produced, ranging from U-214 to U-242 (with the exception of U-220 and U-241). The standard atomic weight of natural uranium is 238.02891 with 99.27% of naturally occurring uranium being the isotope with an atomic mass of 238.

Selected isotopes of Silicon |

|

Selected isotopes of Molybdenum |

|

Selected isotopes of Uranium |

||||||||||||||||||||||||||||||

Nuclide |

|

Protons |

|

Neutrons |

|

Isotopic |

|

Half |

|

Natural |

|

Nuclide |

|

Protons |

|

Neutrons |

|

Isotopic |

|

Half |

|

Natural |

|

Nuclide |

|

Protons |

|

Neutrons |

|

Isotopic |

|

Half |

|

Natural |

22 |

|

14 |

|

8 |

|

22.036 |

|

29 ms |

|

|

|

91 |

|

42 |

|

49 |

|

90.912 |

|

15.49 min |

|

|

|

225 |

|

92 |

|

133 |

|

225.029 |

|

62 ms |

|

|

23 |

|

14 |

|

9 |

|

23.025 |

|

42.3 ms |

|

|

|

92 |

|

42 |

|

50 |

|

91.907 |

|

Stable |

|

14.65% |

|

226 |

|

92 |

|

134 |

|

226.029 |

|

269 ms |

|

|

24 |

|

14 |

|

10 |

|

24.012 |

|

140 ms |

|

|

|

93 |

|

42 |

|

51 |

|

92.907 |

|

4000 y |

|

|

|

227 |

|

92 |

|

135 |

|

227.031 |

|

1.1 m |

|

|

25 |

|

14 |

|

11 |

|

25.004 |

|

220 ms |

|

|

|

94 |

|

42 |

|

52 |

|

93.905 |

|

Stable |

|

9.19% |

|

228 |

|

92 |

|

136 |

|

228.031 |

|

9.1 m |

|

|

26 |

|

14 |

|

12 |

|

25.992 |

|

2.245 s |

|

|

|

95 |

|

42 |

|

53 |

|

94.906 |

|

Stable |

|

15.87% |

|

229 |

|

92 |

|

137 |

|

229.034 |

|

57.8 m |

|

|

27 |

|

14 |

|

13 |

|

26.987 |

|

4.15 s |

|

|

|

96 |

|

42 |

|

54 |

|

95.905 |

|

Stable |

|

16.67% |

|

230 |

|

92 |

|

138 |

|

230.034 |

|

20.23 d |

|

|

28 |

|

14 |

|

14 |

|

27.977 |

|

Stable |

|

92.22% |

|

97 |

|

42 |

|

55 |

|

96.906 |

|

Stable |

|

9.58% |

|

231 |

|

92 |

|

139 |

|

231.036 |

|

4.2 d |

|

|

29 |

|

14 |

|

15 |

|

28.977 |

|

Stable |

|

4.69% |

|

98 |

|

42 |

|

56 |

|

97.905 |

|

Stable |

|

24.29% |

|

232 |

|

92 |

|

140 |

|

232.037 |

|

68.9 y |

|

|

30 |

|

14 |

|

16 |

|

29.974 |

|

Stable |

|

3.09% |

|

99 |

|

42 |

|

57 |

|

98.908 |

|

2.75 d |

|

|

|

233 |

|

92 |

|

141 |

|

233.04 |

|

1.592 e5 y |

|

Trace |

31 |

|

14 |

|

17 |

|

30.975 |

|

157.36 min |

|

|

|

100 |

|

42 |

|

58 |

|

99.907 |

|

Stable |

|

9.74% |

|

234 |

|

92 |

|

142 |

|

234.041 |

|

2.455 e5 y |

|

Trace |

32 |

|

14 |

|

18 |

|

31.974 |

|

153 y |

|

trace |

|

101 |

|

42 |

|

59 |

|

100.910 |

|

14.61 m |

|

|

|

235 |

|

92 |

|

143 |

|

235.044 |

|

7.038 e8 y |

|

0.72% |

33 |

|

14 |

|

19 |

|

32.978 |

|

6.18 s |

|

|

|

102 |

|

42 |

|

60 |

|

101.910 |

|

11.3 m |

|

|

|

236 |

|

92 |

|

144 |

|

236.046 |

|

2.342 e7 y |

|

Trace |

34 |

|

14 |

|

20 |

|

33.979 |

|

2.77 s |

|

|

|

103 |

|

42 |

|

61 |

|

102.913 |

|

67.5 s |

|

|

|

237 |

|

92 |

|

145 |

|

237.049 |

|

6.752 d |

|

Trace |

35 |

|

14 |

|

21 |

|

34.985 |

|

780 ms |

|

|

|

104 |

|

42 |

|

62 |

|

103.914 |

|

60 s |

|

|

|

238 |

|

92 |

|

146 |

|

238.051 |

|

4.468 e9 y |

|

99.27% |

36 |

|

14 |

|

22 |

|

35.987 |

|

450 ms |

|

|

|

105 |

|

42 |

|

63 |

|

104.917 |

|

35.6 s |

|

|

|

239 |

|

92 |

|

147 |

|

239.054 |

|

23.45 m |

|

|

37 |

|

14 |

|

23 |

|

36.993 |

|

90 ms |

|

|

|

106 |

|

42 |

|

64 |

|

105.918 |

|

8.73 s |

|

|

|

240 |

|

92 |

|

148 |

|

240.057 |

|

14.1 h |

|

Trace |

38 |

|

14 |

|

24 |

|

37.996 |

|

90 ms |

|

|

|

107 |

|

42 |

|

65 |

|

106.922 |

|

3.5 s |

|

|

|

242 |

|

92 |

|

150 |

|

242.063 |

|

16.8 m |

|

|

Methods of Separation and Enrichment of Isotopes

Isotope enrichment is the process of concentrating specific isotopes of a chemical element by removing other isotopes. During the last century, a number of different methods have been developed to separate and enrich isotopes. The current separation or

9

enrichment processes are based either on the atomic weight of the isotope, small differences in chemical reaction rates produced by different atomic weights or are based on properties not directly connected to atomic weight such as nuclear resonances.

Diffusion

Often performed on gases, but also on liquids, the diffusion method relies on the fact that in thermal equilibrium, two isotopes with the same energy will have different average velocities. The lighter atoms (or the molecules containing them) will travel more quickly and be more likely to diffuse through a membrane. The difference in speeds is proportional to the square root of the mass ratio, so the amount of separation is small, and many cascaded stages are needed to obtain high purity. This method is expensive due to the work needed to push gas through a membrane and the many stages necessary.

Centrifugal

Centrifugal methods rapidly rotate the material allowing the heavier isotopes to go closer to an outer radial wall. This too is often done in gaseous form using a Zippe-type centrifuge.

A Zippe-type centrifuge relies on the force resulting from centripetal acceleration to separate molecules according to their mass, and can be applied to most fluids. The dense (heavier) molecules move towards the wall and the lighter ones remain close to the center. The centrifuge consists of a rigid body rotor rotating at high speed. Concentric gas tubes located on the axis of the rotor are used to introduce feed gas into the rotor and extract the heavier and lighter separated streams. For U-235 production, the heavier stream is the waste stream and the lighter stream is the product stream. Modern Zippe-type centrifuges are tall cylinders spinning on a vertical axis, with a vertical temperature gradient applied to create a convective circulation rising in the center and descending at the periphery of the centrifuge. Diffusion between these opposing flows increases the separation by the principle of countercurrent multiplication.

In practice, since there are limits to how tall a single centrifuge can be made, several such centrifuges are connected in series. Each centrifuge receives one input and produces two output lines, corresponding to light and heavy fractions. The input of each centrifuge is the output (light) of the previous centrifuge and the input of the following stage. This produces an almost pure light fraction from the output (light) of the last centrifuge and an almost pure heavy fraction from the output (heavy) of the first centrifuge.

Electromagnetic

Electromagnetic separation is mass spectrometry on a large scale, so it is sometimes referred to as mass spectrometry. It uses the fact that charged particles are deflected in a magnetic field and the amount of deflection depends upon the particle’s mass. It is very expensive for the quantity produced, as it has an extremely low throughput, but it can allow very high purities to be achieved. This method is often used for processing small amounts of pure isotopes for research or specific use (such as isotopic tracers), but is impractical for industrial use.

Laser

In this method, a laser is tuned to a wavelength which excites only one isotope of the material and ionizes those atoms preferentially. The resonant absorption of light for an isotope is dependent upon its mass and certain hyperfine interactions between electrons and the nucleus, allowing finely tuned lasers to interact with only one isotope. After the atom is ionized it can be removed from the sample by applying an electric field. This method is often abbreviated as AVLIS (atomic vapor laser isotope separation). This method has only recently been developed as laser technology has improved, and is currently not used extensively.

Chemical Methods

Although isotopes of a single element are normally described as having the same chemical properties, this is not strictly true. In particular, reaction rates are very slightly affected by atomic mass. Techniques using this are most effective for light atoms such as hydrogen. Lighter isotopes tend to react or evaporate more quickly than heavy isotopes, allowing them to be separated. This is how heavy water is produced commercially.

Gravity

Isotopes of carbon, oxygen, and nitrogen can be purified by chilling these gases or compounds nearly to their liquefaction temperature in very tall (200 to 700 feet (61 to 213 m)) columns. The heavier isotopes sink and the lighter isotopes rise, where they are easily collected.

10

The Aerodynamic Separation Process ("ASP") Technology

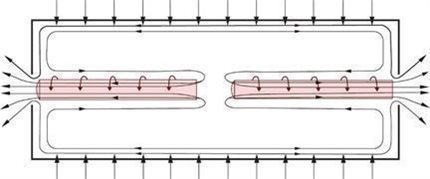

ASP technology is proprietary technology originally licensed from Klydon which succeeds earlier work, first detailed in the scientific media in the mid-1970s, relating to an industrial scale enrichment plant for uranium that was constructed utilizing the so-called “stationary-wall centrifuge”. The original technology was highly energy consuming and was not able to compete on an economic basis with other methods of isotope separation. The innovative development of the ASP technology over the past two decades has culminated in a more advanced separation device that we believe can compete on a commercial scale with other methods of isotope separation. The ASP separation device separates both gas species and isotopes in a volatile state via an approximate flow pattern as shown below.

The ASP enrichment process uses an aerodynamic technique similar to a stationary wall centrifuge. The isotope material in raw gas form enters the stationary tube at high speed by tangential injection through finely placed and sized openings in the surface of the tube. The gas then follows a flow pattern that results in two gas vortexes occurring around the geometrical axis of the separator. The isotope material becomes separated in the radial dimension as a result of the spin speed of the isotope material reaching several hundred meters per second. An axial mass flow component in each tube feeds isotope material to the respective ends of the separator where the collection of the portions of isotope material is accomplished.

The advantages of ASP technology are as follows:

11

ASP Plant Configuration

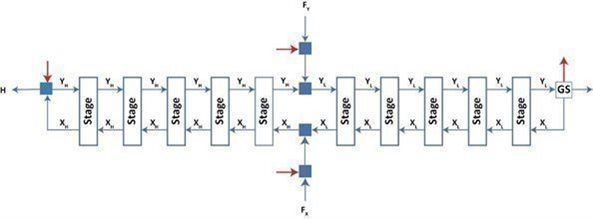

The figure below shows a schematic of an ASP cascade in operation. The cascade consists of several enrichment stages, connected in a 1-up-1-down cascade configuration. The stages can be grouped into segments. (This method of organizing stages is not reflected in the figure)

The bold blue arrows represent flows of the element into and out of the cascade:

Each stage in the cascade is operated in one of two configurations:

The red arrows represent the addition or extraction of carrier gas from the process. The arrows have been added for clarity and orientation, but the mass flows of the carrier gas will be ignored in the rest of the discussion as it pertains to the isotope mass flows only (as represented by the blue arrows). The carrier gas mass flows can be superimposed on any isotope mass balance using the molar mass characteristics of the ASP stages (see below).

The block marked “GS” represents the gas separator: a piece of equipment used to separate the carrier gas from the element of interest to the degree necessary to provide a suitable reflux stream to the tails cascade section.

The blue squares are simply suitable areas where streams can be split or mixed.

An ASP stage is characterized by functions of Y, the flow of isotope in its tails stream. The characteristics of interest are:

Note the following:

12

The cut of an ASP stage can be dynamically adjusted to any value larger than θmin, allowing its operating point to be changed online during production.

All stages in the product cascade section are operated at the same point < XH,YH >, where XH > YH, ensuring that a net backward flow of the process element, H = XH — YH is achieved. This corresponds to a cut of less than 50% and ensures a positive flow of enriched product.

All stages in the tails cascade section are operated at the same point < XL,YL >, where XL < YL, ensuring that a net backward flow of the process element, L = XL — YL is achieved. This corresponds to a cut of more than 50% and ensures a positive flow of stripped tails.

Depending on the production requirements of the cascade the product and tails section operation points can be moved relative to each other during production, obtaining different combinations of H and L (and therefore different feeds F = H + L). The smaller H (or L) is chosen, the closer the product (or tails) section cut moves to 50%. If all stages are operated at a cut of 50%, the cascade is operated at full reflux, no product, tails, or feed streams are present, and the maximum process element concentration gradient will exist.

ASP Technology In Use

The scientists at Klydon had constructed two ASP plants for the enrichment of oxygen-18 and silicon-28 in Pretoria, South Africa, which were commissioned in October 2015 and July 2018, respectively. We believe the success of the enrichment of oxygen-18 and silicon-28 has demonstrated the efficacy and commercial scalability of the ASP technology. We have completed the commissioning phase and are commencing commercial production at our Carbon-14 enrichment facility and our “multi-isotope” enrichment plant, which has its initial production run designated for enriched Silicon-28. We anticipate shipping the first commercial batches of enriched Carbon-14 in mid-2025 and enriched Silicon-28 during the second quarter of 2025.

Quantum Enrichment Technology

Isotopes of every element have unique spectroscopic “signatures” defined by the electromagnetic radiation or “light” absorbed by their atoms from electron transitions. QE separates two isotopes by taking advantage of the slight differences in the transition energy between two isotopes. This method is described as a “quantum mechanics” method. In principle, Quantum Enrichment can separate isotopes of most elements, achieving desired enrichment in a single step.

The atomic vapor laser isotope separation method (“AVLIS”), which is the forerunner of the QE technology, proposed by Letokhov et al. (1977)], has been in progress during the last 45 years. The main efforts during these years were devoted to attempts to get a nuclear fuel for industrial nuclear reactors.

Laser based isotope selective excitation followed by ionization and collection using electro-magnetic fields offers one of the most efficient techniques for isotope enrichment/denaturing. In the laser isotope separation (LIS) process, atoms of the target isotope in vapor stream get ionized after interaction with a tuned laser beam. Ionized atoms are separated from the main vapor stream by electrostatic field. In our Quantum Enrichment facility, a resistive heating system has been designed to evaporate Ytterbium by sublimation at temperature in the range of 500 oC to 700 oC to provide adequate Yb vapor atoms for laser interaction.

13

During the process, the vapor jet comes out from the source to reach sonic speed at the exit plane, then it expands supersonically into vacuum. A thickness monitor reading gives average arrival rate of atomic vapor in terms of thickness per unit time (A/sec).

At the heart of laser-based isotope enrichment lies a proficient multi-step isotope selective photoionization scheme giving optimum selectivity and product yield. Yb has two valence electrons and very few transitions originating from its ground level. Its ionization potential is 6.254eV. This necessitates selection of a three-step photoionization scheme for selective photoionization of its isotopes using the available laser infrastructure supporting visible range of spectrum.

Dye lasers offer the best suitable choice for enrichment process as they suffice to all the requirements of the process like wavelength tunability, high power generation at high repetition rates.

Diode Pumped Solid State Green Lasers (DPSSGLs) with ~3GHz line width in multi-mode operation are used to pump the dye lasers.

The temporal delays between the pulses from the three lasers were arranged to ensure their sequential arrival in the interaction region with delay of several ns.

We believe Quantum Enrichment technology is superior to AVLIS with optimized spectroscopy utilization and superior laser beam shaping.

The key advantages include:

Nuclear Medicine

Nuclear medicine is a medical specialty that utilizes radioactive isotopes, referred to as radionuclides, to diagnose and treat disease. These radionuclides are incorporated into radiopharmaceuticals and introduced into the body by injection, swallowing, or inhalation. Physiologic/metabolic processes in the body concentrate the tracers in specific tissues and organs; the radioactive emissions from the tracers can be used to noninvasively image these processes or kill cells in regions where radionuclides have concentrated.

Other types of noninvasive diagnostic procedures — for example, computed tomography (“CT”) and magnetic resonance imaging (MRI) — can detect anatomical changes in tissues and organs as the result of disease. Nuclear medicine procedures can often detect the physiological and metabolic changes associated with disease before any anatomical changes occur. Such procedures can be used to identify disease at early stages and evaluate patients’ early responses to therapeutic interventions.

Single Photon Emission Computed Tomography (“SPECT”) generates three-dimensional (“3D”) images of tissues and organs using radionuclides that emit gamma rays; the most used radionuclide is Technitium-99m (“Tc-99m”), often referred to as the ‘work-horse’ of nuclear medicine. Individual gamma rays emitted from the decay of these radionuclides (i.e., single photon emissions) are detected using a gamma camera. This camera technology is used to obtain two-dimensional (“2D”) images; 3D SPECT images are computer generated from many 2D images recorded at different angles.

14

Positron Emission Tomography (PET) generates 3D images of tissues and organs using tracers that emit positrons (i.e., positive electrons): for example, fluorine-18 (F-18). Annihilation reactions between the positrons from these radionuclides and electrons present in tissues and organs produce photons. (Two photons are emitted simultaneously for each annihilation reaction and essentially travel in opposite directions.) The photon pairs are detected with a camera having a ring of very fast detectors and electronics. PET images generally have a higher contrast and spatial resolution than do SPECT images. However, PET equipment is more expensive and therefore not as widely available as SPECT equipment. Additionally, most PET tracers have short half-lives (e.g., nitrogen-13 (N-13): 10 minutes, carbon-11 (C-11): 20 minutes, and F-18: 110 minutes), so they must be produced close to their point of use.

Radionuclide therapy can be used to treat conditions such as hyperthyroidism, thyroid cancer, prostate cancer, skin cancer and blood disorders. In nuclear medicine therapy, the radiation treatment dose is administered internally (e.g. intravenous or oral routes) or externally direct above the area to treat in form of a compound (e.g. in case of skin cancer). The radiopharmaceuticals used in nuclear medicine therapy emit ionizing radiation that travels only a short distance, thereby minimizing unwanted side effects and damage to noninvolved organs or nearby structures. Most nuclear medicine therapies can be performed as outpatient procedures since there are few side effects from the treatment and the radiation exposure to the general public can be kept within a safe limit.

ASP Technology for Carbon-14 Enrichment

C-14 is a radioactive isotope of carbon with a half-life of 5,700 years that has a natural abundance of 1 part per trillion. The different isotopes of carbon do not differ appreciably in their chemical properties. This resemblance is used in chemical and biological research, in a technique called carbon labelling: carbon-14 atoms can be used to replace nonradioactive carbon, in order to trace chemical and biochemical reactions involving carbon atoms from any given organic compound.

Carbon-14 could be obtained from waste by-products in certain nuclear reactors. In June 2023, we entered into a multi-year supply agreement with a Canadian Customer for the supply of Carbon-14, which will be produced from our facility that was completed in March 2023. The customer agreed to supply carbon-14 in the form of carbon-dioxide gas as feedstock. We will then convert the carbon dioxide gas into methane under a chemical converting contract entered in June 2023. We will then enrich the methane to greater than 85% C-14 under a tolling agreement, also entered in June 2023. Finally, we will convert the enriched methane back into enriched carbon dioxide under a chemical converting contract. We have received an initial supply of feedstock from our customer and have started the enrichment of C-14. The tolling agreement has a minimum “take or pay” amount of approximately $2.5 million per year, supported by a bank letter of guarantee. In September 2023, we entered into a Memorandum of Understanding (MOU) with the same customer to separate Deuterium and Tritium currently stored at nuclear sites within Canada. The timing and commercial implications of this MOU are subject to future agreement between the parties.

ASP Technology for Silicon-28 Enrichment

Si-28 is a stable isotope of silicon. Isotopically enriched Si-28 is regarded as an ideal host material for semiconducting quantum computing due to the lack of Si-29 nuclear spins. The presence of Si-29 in concentrations above 500 parts per million (ppm) (0.05%) prevents effective performance. The lower the concentration of Si-29, the better a silicon quantum processor will perform in terms of computational power, accuracy and reliability. Unlike traditional centrifuges, which are suited to enriching gases with a high molecular mass, ASP Technology is highly suited to of enriching gases with a low molecular mass such as silane (SiH4), a gaseous compound that contains silicon.

Quantum computers are expected to be thousands or millions of times more powerful than the most advanced of today’s conventional computers, opening new frontiers and opportunities in many industries, including medicine, artificial intelligence, cybersecurity, global logistics and global financial systems.

We have entered into two purchase agreements for highly enriched Silicon-28. The first is with a U.S. semiconductor company. The second is with a global industrial gas company.

Quantum Enrichment Technology for Ytterbium-176 Enrichment

Ytterbium-176 (“Yb-176”) is a stable isotope of ytterbium, that is commonly used to produce Lutetium-177 (“Lu-177”). Lu-177 is a medical isotope used in targeted radionuclide therapy for treating neuroendocrine tumors and prostate cancer. Lu-177 is a medium energy beta emitter (Eβ = 0.149 keV). It is quite damaging, but only deposits its energy within a short range, decreasing collateral damaging effects to normal tissues. It has a half-life of 6.7 days and is compatible with various targeting agents, ranging from short peptides to large biomolecules. The half-life also allows for transport over longer distances and on-site preparation of pharmaceuticals.

15

Lu-177 can be produced in two ways, either directly by irradiation of lutetium-176 (“Lu-176”) or indirectly by irradiation of ytterbium-176 (“Yb-176”). The irradiation of Lu-176 leads directly to Lu-177, while irradiation of Yb-176 will lead to the production of the short-lived intermediate radioisotope ytterbium-177 (“Yb-177”), which decays to Lu-177.

Using the direct method in which Lu-176 is irradiated, the Lu-177 is produced in a matrix (‘carrier’) of Lu-176, because only part of the Lu-176 is converted to Lu-177. This form of Lu-177 is called carried added. Also, the direct method leads to small amounts of the radioactive impurity Lu-177m. This lowers the radionuclide purity of Lu-177 and complicates the radiation protection and disposal of Lu-177 waste in hospitals.

The advantage of the direct production route is that it can create Lu-177 in high quantities by irradiating as little as 1 mg of Lu-176. On the other hand, the desired Lu-177 cannot be chemically isolated from the target material Lu-176, as they are isotopes of the same element. This is problematic as the lutetium administered to the patient should preferably only contain the ‘useful’ Lu-177. If it contains largely ‘useless’ Lu-176, the effectiveness of the treatment will diminish.

The indirect method, where ytterbium-176 is irradiated, does not generate this extra isotope. The Lu-177 is produced in a matrix of ytterbium, which is separated from the lutetium by a chemical process after irradiation. Therefore, it leads to Lu-177 no carrier added. In the indirect production route, Lu-177 differs from the target material Yb-176 and can be isolated chemically in no carrier added (“n.c.a.”) form.

Quantum Enrichment Technology for Uranium Enrichment

We believe our Quantum Enrichment technology is capable of enriching Uranium, which we may be able to commercialize as a nuclear fuel component for use in the new generation of HALEU-fueled small modular reactors that are now under development for commercial and government uses.

Uranium is a naturally occurring element and is mined from deposits located in Kazakhstan, Canada, Australia, and several other countries including the United States. According to the World Nuclear Association (“WNA”), there are adequate measured resources of natural uranium to fuel nuclear power at current usage rates for about 90 years. In its natural state, uranium is principally comprised of two isotopes: uranium-235 (“U-235”) and uranium-238 (“U-238”). The concentration of U-235 in natural uranium is only 0.711% by weight. Most commercial nuclear power reactors require Low Enriched Uranium (“LEU”) fuel which has a U-235 concentration greater than natural uranium and up to 5% by weight. Future reactor designs currently under development will likely require higher U-235 concentration levels of greater than 5% and below 20% (referred to as HALEU – High Assay Low Enriched Uranium). Uranium enrichment is the process by which the concentration of U-235 is increased (see discussion on HALEU demand below).

Separative work units(“SWU”) is a standard unit of measurement that represents the effort required to transform a given amount of natural uranium into two components: enriched uranium having a higher percentage of U-235 and depleted uranium having a lower percentage of U-235. The SWU contained in LEU is calculated using an industry standard formula based on the physics of enrichment. The amount of enrichment deemed to be contained in LEU under this formula is commonly referred to as its SWU component and the quantity of natural uranium deemed to be contained in LEU under this formula is referred to as its uranium or “feed” component. Currently, it is fairly common practice to purchase both the SWU and uranium components of LEU from the enrichment company. Therefore, LEU prices typically consist of three components: SWU, Conversion and uranium ore concentrate.

The following outlines the steps for converting natural uranium into LEU fuel, commonly known as the nuclear fuel cycle:

16

The World is Transitioning to Newer Smaller Reactors

As the world transitions to a decarbonized electric grid, society is gradually decreasing its reliance on fossil fuels and increasing its reliance on “clean energy”. There appears to be bipartisan support for the growth of nuclear energy. Nuclear power, through the operating light water reactor fleet and the deployment of advanced reactors, is poised to be an increasing contributor to carbon free energy in the U.S. and internationally. The United States leads the world in technology innovation with more developers of advanced reactors than any other country.

SMRs are advanced nuclear reactors that have a power capacity of up to 300 MW(e) per unit, which is about one-third of the generating capacity of traditional nuclear power reactors. SMRs, which can produce a large amount of low-carbon electricity, are:

Many of the benefits of SMRs are inherently linked to the nature of their design — small and modular. Given their smaller footprint, SMRs can be sited on locations not suitable for larger nuclear power plants. Prefabricated units of SMRs can be manufactured and then shipped and installed on site, making them more affordable to build than large power reactors, which are often custom designed for a particular location, sometimes leading to construction delays. SMRs offer savings in cost and construction time, and they can be deployed incrementally to match increasing energy demand.

In comparison to existing reactors, proposed SMR designs are generally simpler, and the safety concept for SMRs often relies more on passive systems and inherent safety characteristics of the reactor, such as low power and operating pressure. This means that in such cases no human intervention or external power or force is required to shut down systems, because passive systems rely on physical phenomena, such as natural circulation, convection, gravity and self-pressurization. These increased safety margins, in some cases, eliminate or significantly lower the potential for unsafe releases of radioactivity to the environment and the public in case of an accident.

SMRs have reduced fuel requirements. Power plants based on SMRs may require less frequent refueling, every 3 to 7 years, in comparison to between 1 and 2 years for conventional plants. Some SMRs are designed to operate for up to 30 years without refueling. SMRs are under construction or in the licensing stage in many countries including Argentina, Canada, China, Russia, South Korea and the United States of America.

Within the last five years significant legislation supporting the development and deployment of advanced reactors has been enacted: the Nuclear Innovation and Modernization Act, the Nuclear Energy Innovation and Capabilities Act, the Energy Act of 2020 and the Infrastructure Investment and Jobs Act. In addition, Congress established and funded the Advanced Reactor Demonstration Program which now supports two advanced reactor demonstrations to be deployed within seven years and eight other advanced reactor projects.

SMRs will require a different grade of enriched Uranium

Many advanced reactors, including the majority of the Advanced Reactor Demonstration Program awardees, will require HALEU, and fuel forms very different from those manufactured for the current Light Water Reactors (LWRs). For example, the current generation of LWRs uses fuel enriched to less than 5% uranium-235. In contrast, many advanced non-LWR designs require enrichments between 5% and 20% with most above 10%.

Currently it is not possible to purchase HALEU between 10% and 20% from a commercial enricher in the United States. In the U.S., the infrastructure for the front-end of the fuel cycle for the utilization of low enriched uranium up to 5% U-235 is well defined. The U.S. has mining, conversion, enrichment, fabrication, and transportation capability. However, the infrastructure for

17

producing and utilizing HALEU, in particular enrichments above 10%, is not established in the U.S. The mining and conversion infrastructure are common to all enrichment levels.

In 2020, the DOE selected two companies for awards under the Advanced Reactor Demonstration Program (ARDP) Pathway 1: Advanced Reactor Demonstrations. Both reactor designs require HALEU and can be operational in about seven years. Today, it is estimated that the companies selected for the demonstration pathway will require HALEU for their reactors beginning in the late 2020's to support fuel fabrication ahead of reactor startup. In addition, one of the companies under Pathway 2: Risk Reduction for Future Demonstrations will require HALEU in the 2026-2027 timeframe and other companies in Pathway 2 and 3 of the ARDP will also require HALEU. Privately funded companies are also working to deploy HALEU fueled reactors by the mid-2020s.

The Nuclear Energy Institute (NEI) believes that it is virtually impossible for HALEU to be provided to these companies in the needed quantities and timeframes from DOE inventories or commercial enrichers located in the U.S or Western Europe. Therefore, acquiring HALEU from other international suppliers will be required in the near term to support the larger goal of deploying advanced reactors in the U.S. in a timely manner. Deploying these reactors before 2030 will support climate goals and position the U.S. to be a strong exporter of advanced reactor technology. Per the recent NEI white paper, a robust domestic HALEU infrastructure is necessary to support both the domestic deployment of advanced reactors and the export of U.S. advanced reactor technologies requiring HALEU.

In a letter to the DOE captioned “Updated Need for High-Assay Low Enriched Uranium” dated December 20, 2021, the NEI provided an estimate of what U.S. HALEU demand may be during the next 15 years by companies denoted A to J:

Estimated Annual Requirements for High Assay Low Enriched Uranium to 2035 (MTU/yr)

Company |

|

A |

|

|

B |

|

|

C |

|

|

D |

|

|

E |

|

|

F |

|

|

G |

|

|

H |

|

|

I |

|

|

J |

|

|

Total |

|

|

Cumulative |

|

||||||||||||

Year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

2022 |

|

|

0.1 |

|

|

|

0.4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0.2 |

|

|

|

|

|

|

1.1 |

|

|

|

0.0 |

|

|

|

1.8 |

|

|

|

1.8 |

|

|||||

2023 |

|

|

0.1 |

|

|

|

3.1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4.4 |

|

|

|

0.1 |

|

|

|

7.7 |

|

|

|

9.5 |

|

||||||

2024 |

|

|

1.0 |

|

|

|

5.6 |

|

|

|

0.2 |

|

|

|

3.0 |

|

|

|

|

|

|

|

|

|

1.5 |

|

|

|

|

|

|

6.6 |

|

|

0.1 |

|

|

|

18.0 |

|

|

|

27.5 |

|

||||

2025 |

|

|

1.0 |

|

|

|

3.8 |

|

|

|

0.4 |

|

|

|

3.0 |

|

|

|

|

|

|

5.0 |

|

|

|

|

|

|

|

|

|

11.0 |

|

|

1.6 |

|

|

|

25.8 |

|

|

|

53.3 |

|

||||

2026 |

|

|

1.0 |

|

|

|

15.1 |

|

|

|

|

|

|

4.9 |

|

|

|

|

|

|

10.0 |

|

|

|

2.0 |

|

|

|

24.2 |

|

|

|

13.2 |

|

|

|

1.7 |

|

|

|

72.1 |

|

|

|

125.4 |

|

||

2027 |

|

|

1.0 |

|

|

|

26.5 |

|

|

|

|

|

|

7.9 |

|

|

|

|

|

|

|

|

|

4.0 |

|

|

|

24.2 |

|

|

|

13.2 |

|

|

|

1.9 |

|

|

|

78.7 |

|

|

|

204.1 |

|

|||

2028 |

|

|

1.0 |

|

|

|

37.8 |

|

|

|

|

|

|

16.6 |

|

|

|

|

|

|

13.0 |

|

|

|

23.0 |

|

|

|

24.2 |

|

|

|

13.2 |

|

|

|

2.0 |

|

|

|

130.8 |

|

|

|

334.9 |

|

||

2029 |

|

|

1.0 |

|

|

|

26.3 |

|

|

|

1.8 |

|

|

|

30.5 |

|

|

|

17.0 |

|

|

|

18.0 |

|

|

|

14.0 |

|

|

|

24.2 |

|

|

|

16.5 |

|

|

|

2.4 |

|

|

|

151.7 |

|

|

|

486.6 |

|

2030 |

|

|

1.0 |

|

|

|

34.4 |

|

|

|

1.8 |

|

|

|

40.4 |

|

|

|

46.0 |

|

|

|

18.0 |

|

|

|

30.0 |

|

|

|

24.2 |

|

|

|

16.5 |

|

|

|

2.7 |

|

|

|

215.0 |

|

|

|

701.6 |

|

2031 |

|

|

23.0 |

|

|

|

42.5 |

|

|

|

6.2 |

|

|

|

53.0 |

|

|

|

29.0 |

|

|

|

22.0 |

|

|

|

33.0 |

|

|

|

24.2 |

|

|

|

16.5 |

|

|

|

2.9 |

|

|

|

252.3 |

|

|

|

954.0 |

|

2032 |

|

|

35.0 |

|

|

|

52.9 |

|

|

|

12.5 |

|

|

|

67.6 |

|

|

|

46.0 |

|

|

|

40.0 |

|

|

|

50.0 |

|

|

|

48.4 |

|

|

|

19.8 |

|

|

|

3.1 |

|

|

|

375.3 |

|

|

|

1,329.2 |

|

2033 |

|

|

47.0 |

|

|

|

63.5 |

|

|

|

32.2 |

|

|

|

82.1 |

|

|

|

46.0 |

|

|

|

32.0 |

|

|

|

80.0 |

|

|

|

48.4 |

|

|

|

19.8 |

|

|

|

3.2 |

|

|

|

454.2 |

|

|

|

1,783.4 |

|

2034 |

|

|

58.0 |

|

|

|

76.1 |

|

|

|

62.4 |

|

|

|

96.7 |

|

|

|

46.0 |

|

|

|

36.0 |

|

|

|

80.0 |

|

|

|

48.4 |

|

|

|

19.8 |

|

|

|

3.7 |

|

|

|

527.1 |

|

|

|

2,310.5 |

|

2035 |

|

|

70.0 |

|

|

|

90.9 |

|

|

|

96. |

|

|

|

112.4 |

|

|

|

91.0 |

|

|

|

29.0 |

|

|

|

50.0 |

|

|

|

48.4 |

|

|

|

22.0 |

|

|

|

4.1 |

|

|

|

613.8 |

|

|

|

2,924.3 |

|

Notes:

18

Quantum Enrichment Technology is ideally suited to the production of HALEU

We believe that we are in a very different position to many of the entrenched domestic and international enrichers. Our innovative isotope enrichment process has a number of advantages over traditional gas centrifuges and other novel approaches currently being explored by other companies: cheaper in capital expenditures, faster in construction, more flexible in design and location.

We estimate that the capital cost of constructing a Quantum Enrichment technology plant for uranium enrichment is approximately 75% cheaper than that of a traditional gas centrifuge enrichment facility. Our manufacturing plants are modular, so our construction time is likely faster and more flexible than competing technologies. Our enrichment facilities are smaller than traditional gas centrifuges which means we can place them near fuel fabrication facilities for enhanced security of production and transportation. Our operating costs of enriching uranium to 15.5% - 19.75% U-235 should be comparable to or cheaper than costs for other methods of uranium enrichment.

The table below represents management’s estimated comparison of the Quantum Enrichment technology with a traditional gas centrifuge.

|

|

Quantum Enrichment Technology Plant |

|

Gas Centrifuge |

Separation mechanism |

|

Enhanced resonant multiphoton ionization |

|

Differential diffusion |

Capital Cost per plant |

|

<$100 million |

|

>$800 million |

Energy use (kWh) per SWU |

|

<40 |

|

50-240 |

Construction time |

|

2-3 years |

|

2-3 years |

Levelized cost per SWU* |

|

<$50 |

|

$140 |

* for enrichment from 0.71% U235 to 5% U235

We are in the process of commissioning and commencing commercial production at our Ytterbium-176 enrichment facility using the Quantum Enrichment technology in Pretoria, South Africa. We received a manufacturing permit for this facility from the South African DMRE during 3Q 2023. The construction of this plant will provide us with valuable experience in the construction of Quantum Enrichment technology facilities in the future. Many of the control systems, compressors, lasers and hardware used in a uranium enrichment facility would be similar to parts used in this ytterbium-176 enrichment facility.

We expect the construction of a Uranium Enrichment facility would take approximately 30 months and the production volume would gradually ramp up to the final capacity of 20 metric tons per year. Importantly, subject to licensure, we believe we can produce commercial quantities of HALEU by 2027 to meet the anticipated demand from the advanced reactors currently in development. We believe that we can supply HALEU at a price lower than the HALEU currently imported from international enrichers and considerably lower than any potential domestic supply that may evolve.

Intellectual Property